New 529 Plan Rules 2025: How the OBBBA Helps Families Save for College and Retirement

WRITTEN BY: Carrie M. Leontitsis, J.D.

New 529 Plan Rules You’ll Want to Know: How the One Big Beautiful Bill Act Helps You Save Smarter for College and Retirement

If you’re a high earner juggling the dual goals of building your retirement nest egg and investing in your children’s future, the new 529 rules from the One Big Beautiful Bill Act (OBBBA) could be a game-changer for your planning strategy.

Signed in to law on July 4, 2025, the OBBBA updates to 529 college savings plans make them more flexible than before, helping you avoid wasted dollars, reduce taxes, and even create another avenue for long-term retirement savings.

What’s the Benefit of a 529?

529 plans have traditionally been used by parents and other family members to create tax advantaged college savings accounts for younger beneficiaries. Each individual student is the beneficiary of their own account, with an account owner/custodian (usually the parent or guardian) who manages the account.

While there is no federal income tax deduction for contributions to the accounts, the earnings grow tax free, and withdrawals for “Qualified Educational Expenses” are also tax-free. Also, many states with a state income tax offer either deductions or credits for contributions.

Prior to the OBBBA, the funds needed to be used primarily for college, university, and trade school costs, with other benefits:

- Could be used for up to $10,000/year for K–12 tuition (added in 2017), however not all states allow for K-12 expenses.

- Unused 529 funds (up to $35,000 lifetime) could be rolled over to a Roth IRA for the beneficiary, under certain conditions.

- Could also be used to repay up to $10,000 in student loans (added in 2024) for the beneficiary and their siblings (lifetime limit per individual).

- Unused funds could also be withdrawn with a 10% penalty, and taxed at the beneficiary’s ordinary income tax rate, or transferred to a different qualified beneficiary for their use.

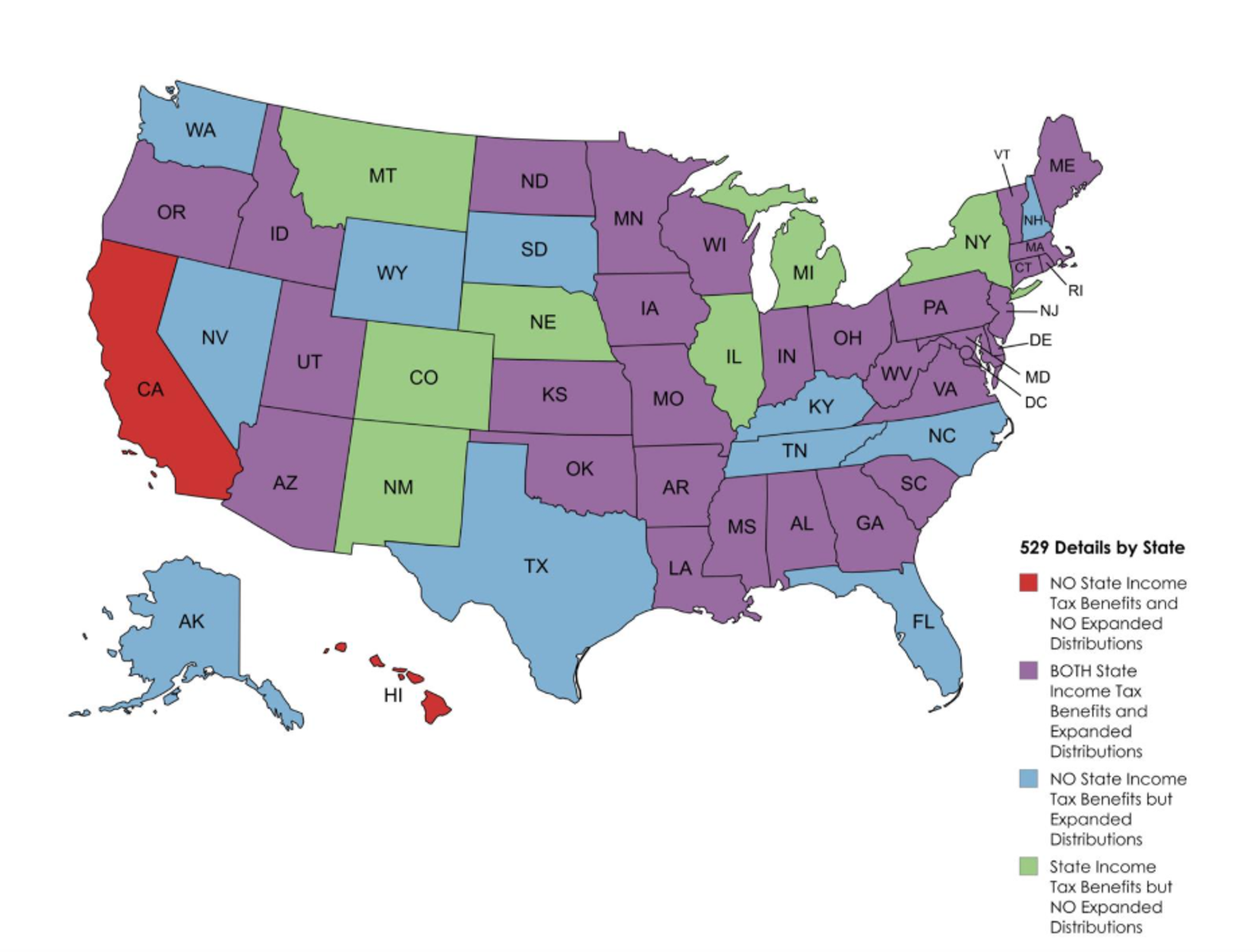

Tax Benefits By State

This map helps show which states give a state income tax benefit and which states have expanded the definition of Qualified Educational Expenses to include K-12 costs.

New with 529s under the OBBBA? While the provisions related to the Roth IRA rollover benefit, student loan repayment options, and taxes and penalties on non-qualified withdrawals remain the same, the OBBBA changes mean your 529 can also now: Use funds for additional college or other career advancement expenses such as professional licensing and certification fees, tutoring, miscellaneous fees, books, exam costs, and supplies for federally recognized work programs and military career advancement, and continuing education credits...not just traditional tuition, books, and fees.

In states that have expanded distributions to K-12 expenses, be used for an increased annual distribution of up to $20,000/year, and used for curriculum materials, fees for nationally standardized tests, books and other instructional materials, dual-enrollment fees for college courses taken in high school, online educational materials, tutoring or educational classes outside the home, and new specialized strategies designed to support students with disabilities

Take advantage of inflation-adjusted annual gift tax exclusion amount and the extended and increased lifetime gifting limit, so that you can contribute more without triggering gift tax reporting or gift tax liability.

Why HENRYs Should Care

For high-earning families still in the wealth-building stage, 529 plans now offer more than just college savings. They’ve become a multi-purpose tool for tax-smart investing, intergenerational wealth planning, and even indirect retirement savings. These changes help ensure your hard-earned dollars are always working...whether your child goes to med school, starts a business, or ends up with a Roth IRA head start. What’s Next for Your Plan? If you’re contributing to a 529 or considering one, now is the time to: Revisit how much you’re saving and for whom. Look at how the Roth rollover option can fit into your family’s long-term financial plan. Explore strategies to maximize the tax and growth benefits alongside your retirement savings.

At Drucker Wealth, we specialize in helping our clients align college savings, retirement goals, and tax strategies into one cohesive plan.

Schedule a Right Fit Call with us today to see how we can help you, too.